7 + 1 + 7 + 3.5 =

These numbers used to mean 18.5 to me. Now thanks to a bloke named Phillip J Anderson, it is the number of years in a full property cycle.

After GFC I went on the hunt for information. I am a bit of an information junkie and wanted to know about the financial downturn and what caused it.

Everybody had an opinion and none of them were really based on anything other than the experiences they were exposed to in their job or life situation. A financial analyst wrote that the GFC was about the market confidence being low, a property broker said it was the lack of credit supply, a trader said it was packaged loans sold to institutions.

None of this was really pieced all together for me until the middle of 2013 when I discovered Phillip J Anderson’s work on real estate cycles.

Phil is an Aussie economist who is definitely a non-conformer. He does things differently and one of the big differences is that Phil reckons that all markets are driven by the Real Estate market.

Hang on, an economist saying that property is the driver?

I had to read more.

I had to see if this was the key to understanding the property markets and being able to guide clients through the cycles.

Suffice to say I have spent the last 3 years gathering as much information about Phil and his work including becoming a subscriber to his services. I needed to know this was the real deal before I exposed my clients to a totally new way of thinking.

I am now a sold out convert…

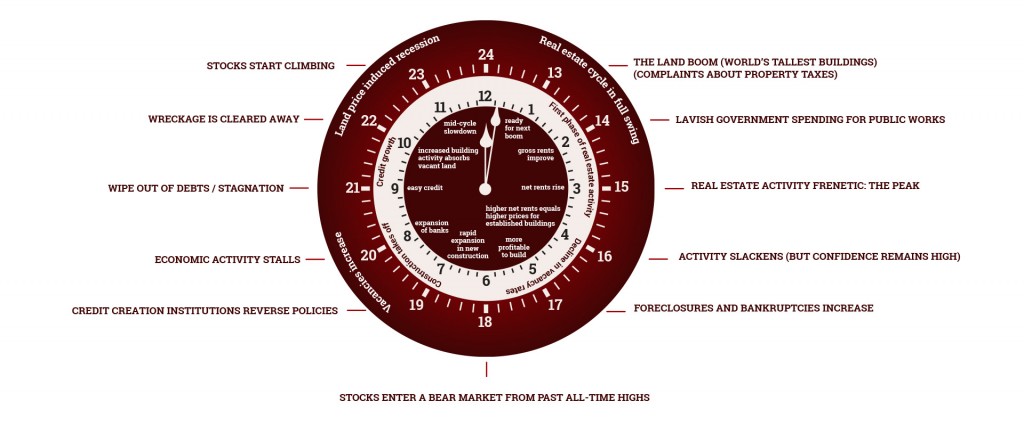

Now all our information at Real Property Advice comes through the PJA filter first. We line up any news to see where that sits on the 24 hour Property Clock as designed by Phil J Anderson.

Any development sites we work on, or property purchased, all has to fit within the correct position on the property cycle timing.

We now help clients gather information and act in total confidence of the macro environment in which we are operating.

It needs to be noted, this system is not date specific but rather time specific. There is a big difference. If you try to run by a specific date you will get caught…

Here is Phil’s cycle in overview:

7 good years

1 negative year

7 good years

3.5 negative years

Phil found that this 18 year cycle has been happening since the 1700’s!

Yep he has tracked it back all the way till the land booms of the U.S. property market in the very early years.

On the dot, 18 years from low to low, high to high, 18 years every time.

If you want to know what is going to happen in Real Estate you just need to do some simple math.

Negative years (3.5 down) 2008 (GFC) + 3.5 = late 2011

Growth years (7 up or sideways) 2011 + 7 = 2018

Negative Year (1 down) 2018 +1 = 2019

Growth years (7 up or sideways) 2019 + 7 = 2026

Next big crash (3.5 down) 2026 + 3.5 = 2030

As you can see, if this is right, you now have a road map of when to invest and when to exit.

I will leave that with you to consider and to check out Phil’s website at www.phillipjanderson.com to make your own mind up about his claims.

We will explore more of Phil’s concepts in future articles.

If you would like to know more about what we can do for your property portfolio or how we apply Phil’s work to the local property market, contact us via email or phone the office on 1300 66 77 89.

Since 2004 Scott Northcott has been helping people buy the best properties for their needs at prices that simply speak for themselves.

Scott has been instrumental in bridging the gap between financial planning and traditional real estate transactions through his property advice model. By carefully considering his clients’ goals and planning for market changes via demographics and trends, Scott designs a future proof outcome not only specific to the client’s needs but dynamic in its execution with performance indicators and exit strategies built in.

22 Comments.

Thanks Scott great breakdown. Surely the ‘up’ or ‘sideways’ 7 years means property prices (which I see as having risen very high where I’ve worked in last 2 years – Qld) could go sideways before the negative 1 year & not necessarily continue to rise. Time to buy? Knowing there is another 7 still to go. What do you feel about the big 4 having large 90+ days defaults in their current annual / six monthly reports and the effect on property & rates.

Hi Carmel,

Thanks for your comment. The breakdown of the cycle is very much a generic guide. As such some locations will rise more than others and also before or after others. With that in mind, what you say is correct. Essentially the ‘upwards’ part of the cycle simply means ‘not downward’ and therefor a sideways movement into a downturn is totally possible.

Time to buy is more based around when you need to sell. I am working on time based colour system that might help people decide when to buy based on when they are looking to sell again. We are still buying for clients at the moment as long as they have a greater than 5 year hold time or are buying a project.

Re the big 4, i find it hard to believe much of what is spun from their media department. Didn’t they all just post big profits? I think it was $15bil combined for the first HALF YEAR?

Poor banks, how do they handle their 90 day defaults.

In all seriousness, they are promoting the things they want in the media. Arrears might be up but so is profits. Maybe there is just more money around to be behind in arrears and also to be profitable from. This will be driven from loans to assets and there carries on the cycle..

Thanks for connecting.

Scott

So then how do you explain property prices in Sydney going up over the 2008-2011 period, isn’t it supposed to be 3.5 years down??

Hi Paul, thanks for joining the chat. You make a very valid point about a market that has not performed exactly like a clock cycle says it might. In fact the Sydney market did lead our (Australian) downturn and recovery, and it looks like perhaps it will do the same coming into the next phase of a cycle.

Sydney prices did take a hit from 2007 – 2008, but compared to other parts of the country and the world, it was not much. There was a 6% price drop in 2008 between March and December, which in reality, is barely worth talking about, especially if you didn’t need to sell you property in that time.

The other thing to note is that no 2 cycles are identical. At the time this can cause confusion or even over confidence in some regards but the advantage of hindsight will show a cycle taking place.

There are a few people online giving argument as to why Sydney did not perform like the other cities in Australia and one such argument is that it was due to

‘growth in the city’s house prices was much softer than other cities for much of the 2000s… this graph, which shows the ratio of Sydney homes to those in other cities was below-average for much of the decade.’

I can’t post the graph but here is the link http://www.smh.com.au/business/the-economy/six-graphs-that-show-why-we-may-not-need-to-panic-about-housing-20160225-gn3mnu.html

In every cycle government tries to intervene to make the effects less hazardous to our financial heath. Sometimes things work better than other times and external market influences also can play a part.

My review of the last 8 years in Australian property is that we have been very lucky compared to other places, but even saying that, not all towns or cities in our country performed the same way or very few like Sydney.

I would always review the Property Cycle clock within the context of the overall market and also within the context of the city you are transacting in.

Thanks again Paul for commenting.

Cheers

Scott.

In my opinion this phenomena can be explained by adding a layer of complexity to the 18 year cycle theory.

As Phil Anderson correctly predicted, the exponential growth of China would mean Australia would not see a major downturn or sustained housing correction. However in his ‘Boom times’ article for moneyweek of 2014 with Akil Patel they also (correctly) suggested 2015/16 would see a cyclical downturn in the Asian/emerging markets, and following China’s 2015 stock market correction the still spiraling private debt and ever weakening currency tells us the story here is far from over, and imo contagion will follow across the region probably gaining significant momentum as soon as next year.

The question then is, can Australia dodge another bullet over the next 1-3 years? Sorry to put a cat among the pigeons but here I think Phil Anderson may have been wrong-footed by his belief in long term cycles in commodity prices and that the Western cycle would recover sufficiently to sustain Oz’s ‘miracle’ recession free status till 2026. I’m in the UK, but Oz is certainly an economy to keep an eye on!

Hi Mark,

Thanks for joining in.

I think you have accurately summed up the situation. Can Australia dodge another bullet? Good question.

I know of people who would say we didn’t dodge the last one, but as a general overview, I would agree that we did.

The Anderson Property Clock says we are due for a mid cycle slow down in the next couple of years, so yes it lines up with your 1-3 year timeframe too. If that is the case, then what does this mean and what can anyone do to prepare for it?

Lets say this slow down is on time and happens. What would be the normal response from government and community? if stimulus happens and then the slow down ends, everyone gets cocky and that drives the last half of the property cycle to even greater heights, right up till 2026.

If the mid cycle goes deep and recovery does not happen, then Anderson and historical data is wrong and we are looking down the barrel of the next property crash.

Either way, when this happens, I see good buying times for our cashed up clients. The trick will be to know how long into the ‘downturn’ do you wait till you buy in?

Have a great day over in the UK.

Scott.

Where would the best to purchase a investment property in Melbourne for up to 350K

Hi Hayden,

Thanks for connecting with us. For specific questions about your situation or locations etc, it is best to email the office via:

advice @ propertyadvice.com.au

We will look out for your email and get back to you with ways we can assist your inquiry.

Thanks

Scott.

We have recently sold our home in Melbourne and don’t know whether to buy straight away or rent for a year or two and then buy?

Hi Nico,

Thanks for connecting with us. For specific questions about your situation or locations etc, it is best to email the office via:

advice @ propertyadvice.com.au

We will look out for your email and get back to you with ways we can assist your inquiry.

Thanks

Scott.

This is interesting, im wondering , if this ‘cycle’ is correct where is the “money’ going to come from to fund the growth. I think there is a ‘black swan’ that we are missing comparing this ‘cycle’ to historical trends and that’s the internet. The internet brought ‘globalisation’ which is now appearing to create excess competition, therefore , market over-supply and reduced ‘total cash’ in industries. Individuals appear to have less over-all household liquidity ..the credit market is allegedly contracting so continued credit issuing cant be the answer yet the cycle says otherwise. Govt intervention would be hard given our huge debt levels?

Hi Jake,

Thanks for your comment. I totally agree that this and every cycle will have different components to it, and tech/internet is one of those in this cycle. However i will say, in every past cycle the people in it (you and me) had a tendency to view it though a set of blinkers that said, this cycle will be different.

I think it will be different but more of the same, if that makes sense.

In regard to ‘Where will the money come from?’ banks will always be out to provide funding and don’t forget, when they write loans that is new money. Banks don’t use cash deposits sitting in accounts to provide you funding, they create new money when drafting a loan, therefore the expansion in the money supply continues.

All that means is while people are taking out loans and a lot of that new money ending up in real estate, the property cycle will continue to tick over and generally each boom is larger than the last, meaning each bust is larger too.

Thanks for joining the conversation.

Cheers

Scott.

Hi Scott,

Is there a chart of Australian Real Estate that show the cycles? If so, how far in time does it go back? Would love to see how accurate a picture it depicts.

Many thanks.

Hi Glenn,

Thanks for your comment. The best data I have in regards to the overall property clock would be Phil’s book, the Secret Life of Real Estate and Banks. I got my copy online from booktopia, but I think amazon has it too.

It outlines all the property cycles for the past 150 plus years and then you line it up with Australia after that. Aus is about 1 year behind the U.S. in its cycle and we get to see what is happening almost a year ahead of time, because of that fact.

You need to balance the master or overall property cycle with individual cycles based on local happenings. For example the east coast of Aus has performed right on scheduled for the clock as displayed in this article, but Perth and Darwin have not done anything like it. Nor has Mackay, Rockhampton, or Townsville to name a few places in QLD. And don’t even mention mining towns like Moranbah or Blackwater.

So all those local factors need to be taken into consideration too.

I would suggest getting a copy of Phil’s book and review his take on the matter.

Cheers

Scott.

Hi Scott,

The big question is now, will 2019 be a mid cycle correction, or a full recession. The clock suggests the timing is right for a mid cycle recession. However, and I hate to go down the “this time is different” path, the banks have tightened credit off the back of the royal commission. They are lending less and declining many applications. This has reduced the buyer market and caused house prices to decline. This won’t change anytime soon. If labour gets elected next year, their negative gearing changes will add fuel to the fire. The govt sees this and has removed restriction on interest only investor loans. But it’s too late. Investors won’t buy in this uncertain market, and they can’t get past the banks new strict lending criteria. Although some might try to jump in and capitalise on the “grandfathering” of the negative gearing changes.

So I’m in two minds. Yes the timing lines us up for a mid cycle correction. But the tightening of lending, level of debt, falling house prices, and little room to reduce rates further tends to paint the picture we are heading into a recession.

Hi Dehran,

Thanks for your comment.

I see all the points you mentioned and agree, will this time be different? I cant help but think for those of us who subscribe to the property cycle concept, that every time this part of the cycle happens, we might ask the same thing.

I have…

To me I relate it to flying a plane in clouds. As soon as you enter it can feel like you are banking, but you aren’t and if you respond to that feeling then you will crash. However if you follow your instruments you are fine.

I see Phil’s clock and cycle as an instrument, and I need to trust it when it get cloudy like now..

Hi Scott

It looks like it’s now 18 months since your article and we have seen some downwards movement in prices in Sydney and Melbourne but not so much in Brisbane. I’m just wondering if you like to share your thoughts on 2019.

Regards

Peter

Hey Peter,

Thanks for stopping by. I have just done a video on my forecast for 2019, in a very general sense and will be posting up here very soon.

However to surmise, I think this year is going to continue to be bad for Sydney and Melbourne, Brisbane will do OK as more southerners come up this way for some sunny action. But it wont be immune. I think Brisbane may see trouble at the end of this year early next.

Brisbane normally peaks lower than Sydney and Melbourne, follows them after into a downward, and ‘most’ times does not have as long a down time. this is not cause Brisbane is special but more that Sydney and Melbourne have come out of the other side of their downwards cycles and begins to lift other places back up.

I actually think the actions and findings from the Royal Commission have just given the big banks the ammunition to power the next stage of the upwards property cycle, whenever that happens. If mortgage brokers are killed off then, look out public, it will be loans aplenty from the big banks.

Cheers.

Hi Scott, Everyone is talking up SE QLD for some time and it seems inner ring has only done well. People are now talking up middle/outer ring, I don’t see product in Logan as an example doubling like last boom especially the declines Sydney is experiencing and Melbourne following…

Hi Michael,

Thanks for connecting.

We do a lot of work in SEQ and I agree with you on everyone talking it up. Really Brissy is the poor cousin of Sydney and Melbourne in that it does things slower and not as extreme. So in that regard, it is a potentially less volatile than (especially) Sydney, with SEQ having smaller peaks and smaller troughs (cause the peaks weren’t as high).

This gives the impression of more stability.

Perhaps this is why people talk it up? I dont know…

In regards to Logan, and for that matter Ipswich, Caboolture and other lower priced areas with lots of land, I can’t see prices moving in the way you mentioned either.

The simple fact is that there is acres of land to bring on to the market and therefor no land supply pressures (other than manufactured ones) meaning growth will be be less.

This does not mean I am against lower priced property, in fact the opposite is true. I always like to buy the cheapest placed I can within a decent area, but you have to remember that land supply always effects prices.

So we don’t buy in just about all those areas I mentioned above, simply on land supply.

Have a great day.

Hi Scott,

Thanks for the reply. What areas do you see good upside the next 3 years in SE QLD?

Hey Michael,

Look for infrastructure planning and then announcements and delivery. Using the public’s purse to increase the value of a property you own, is a super smart way to go. Brisbane is till a city that most people like to ‘live just out of’ so the inner North, West, South and East are good places to look. Just don’t get caught up in the idea that you must have CBD property in Brisbane.

If price is an issue then you simply need to look further out and balance your age vs condition vs price vs rent component of the purchase.

Hope that helps a little.

Scott.