It’s not much use having an awesome roof, if you have nothing holding it up.

This statement is very relevant to scribbles today. The difference between tin on the ground and tin as a roof, is what’s holding it up.

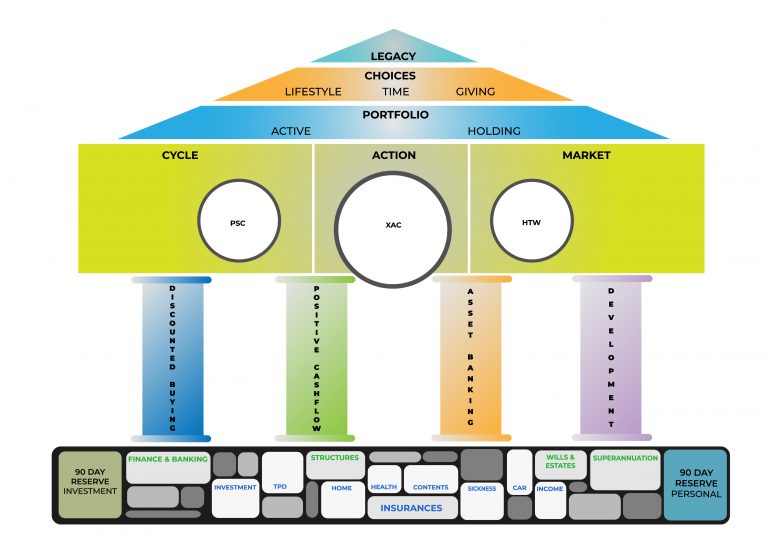

Walls, supports, structure, posts or pillars.

Further to our last scribbles on the Palazzo De Wealth, today I will expand on the importance of the pillars of investment and how they work together for overall balance.

(If you have not read that article, take a look here as this post won’t make much sense without its info.)

The four pillars are:

1) Discounted Buying

2) Positive Cashflow

3) Asset/land banking (speculation)

4) Development (modification of asset)

Discounted Buying

The first time most people buy property, is usually their first home. This is changing slowly but in general we all scrimp and save to get that home, not of our dreams.

One of the priorities for me when buying my first home (and due to my job, every purchase thereafter) was to get the best price I possibly could. In fact the price I bought my first home for, ended up being one of the cheapest sales in the area ever made.

When buying my current home, we ended up with a 20% discount from the list price. Like you, I enjoy getting a deal on things and bargains.

Yes this is a good thing, however it is not fully what this pillar is about.

Discounted buying is more than getting a good price. It is buying a discounted / distressed asset below its previous market value due to the market action of that region at that time.

Let me put it another way.

If you had to buy an investment property, would you prefer to buy one on sale at a discount, or at slightly off full price due to a hot market?

So there is two levels of discounted buying.

1) A negotiated discount off the property price/market value

2) A market discount due to depressed/suppressed market conditions at that time.

You may or may not be able to negotiate a good deal (number 1) but if you know where to look and what to research, you can always take advantage of number 2.

Market condition discounts are usually much larger than any negotiated discount ever is.

Go with the easy outcome and research depressed / suppressed areas and strike, at a discount.

Positive Cashflow

The life blood of your financial world. Cashflow is king, is how the saying goes. After honing your skills and buying at a discount, the next stage is refining your cashflow.

This pillar is what springboards you into the following pillars, as cashflow makes borrowing more possible and comfortable.

If you only ever get to the first two pillars, that’s ok. Creating equity through discounted buying and then adding positive cashflow into your portfolio is nothing to scoff at.

(The danger is when you start at the other end of the pillars without having your strong basics sorted)

It should be noted, positive cashflow can be ‘passive’ or ‘active’; although I don’t think much in life is ever totally passive.

An example of active cashflow might be building a duplex and selling the finished units upon completion. Overall that year, you had a positive cashflow result.

Asset / land banking – (speculation)

The next stage in your investment portfolio is taking some risk. Speculation and gut feel is what this stage is all about.

Acting on a whim is not what I mean, but calculated risk analysis is the order of the day.

At this point you will have some good equity, and decent cashflow in your assets. This allows you to borrow well and take a little bit of defined risk.

Maybe it is an older house that has the potential to be cut up later, or maybe it is an unused farm. Perhaps it is a duplex with zoning for medium density to make 4 townhouses.

Whatever it might be, land banking is pretty much anything purchased that has the potential for a manufactured or above market, uplift at a later stage.

It is important to note, that landbanking is separate from the next pillar, Development. This is because landbanking has a different risk profile and is not the action of changing the asset. It is the action of speculating value uplift through potential market or property activities.

Development – (modifying the asset)

The most risky and potentially profitable pillar is development. Covering everything from small renovations, industrial construction, land subdivision and anything else you can imagine.

The actions of this pillar are to take a property (the asset) and change it, while doing so, increasing the value of the asset more than it has cost you to perform the changes.

That difference is your development margin.

Development large or small has risks. Most times the size of the development aligns with both the risk and rewards, but not always.

You need a great team at this stage and some strong foundations behind you if you are going to go it alone.

As you can see the pillars work together to form a strong platform for the next pillar and the actions you need to take to secure your financial future.

Trying to do development without equity and before you get good at research is a recipe for disaster.

Don’t go hunting for land banking opportunities until you have your cashflow sorted.

One pillar builds upon your foundations and the other pillar before to make sure your structure holds together when the storms come.

We all know that happens, usually when we least want it to.

It is my experience that if you prepare for the bad times, they seem to come less frequently.

Having a strong investment plan and structure is part of that wise preparation.

So what are you waiting for?

If you want to secure your financial future using property, then contact us here or call now on 1300 66 77 89.

Since 2004, Scotty North has been helping people buy the best properties for their needs at prices that simply speak for themselves.

Scotty has been instrumental in bridging the gap between financial planning and traditional real estate transactions through his property advice model.

Scotty North is a Qualified Property Investment Advisor (QPIA), with accreditation’s in financial planning, mortgage broking and real estate.

By carefully considering his clients’ goals and planning for market changes via demographics and trends, Scotty designs a future proof outcome not only specific to the client’s needs but dynamic in its execution with performance indicators and exit strategies built in.