Infinite Equity

“All you need to do is buy 10 properties and refinance one property each year, pull out money to live on and you never need to worry about money or tax again.”

In 2003/4 Mortgage Managers were the cool thing.

Taking a more active approach than a bank or a broker (supposedly) Mortgage Managers help you achieve debt reduction quicker through a handful of ‘Special Strategies’.

This week a mate and long-time reader of Scribbles (let’s call him Alex), emailed me a question. Alex’s question went like this:

Hi Scotty,

Been tracking with your newsletter and picking up some really great knowledge!

Working off one of your tips on investment loan reduction, I wanted to pick your brains on a strategy I recently was exposed to – I am sure you get asked this a thousand times…

Basically, the idea is to build a property portfolio over a decade with interest only payments and live off equity. This particular group advocates never paying off your investment loan to maximise available cashflow.

“Why pay off your $2m debt when you have $8m in equity?”

What’s interesting is that they suggest taking a $1m+ facility when you have enough equity and live off that at approx 5% interest rate instead of the marginal tax rate.

What’s your take on this?

Regards Alex.

Alex has come across one of those ‘Special Strategies’, dug up, dusted off, repackaged and put back out to market.

That is the idea of Infinite Equity.

This strategy (excuse me while I choke) calls for the purchase of a number of investment properties using equity from the ones before. Once you hit a predetermined number, say 10, then you move from purchase mode to retirement mode.

During this time, you refinance (to 80% LVR) the oldest property, number 1, and draw down funds on which to live for the year.

In year 2, you refinance (again to 80%) property number 2 and draw down funds for living.

And so it goes, every year, forever..

What could possibly go wrong?

Pros and cons

I am not saying that it is bad to buy 10 properties, nor is it bad to refinance the property before to help buy the next one.

I am saying this strategy has holes.

What is wrong with the Infinite Equity model?

It assumes constant and lineal growth, costs, and income.

It assumes you always have the ability to borrow and take on debt.

It assumes the banks desire to lend, and their criteria are constant.

It assumes low interest rates that don’t kill your cashflow.

This is far from what actually happens in the market.

Growth is not lineal and nor are costs and serviceability. The long-term average might be that property doubles every 10 years, or it might not.

In the years there is not lineal growth, then the ability to refinance may not even be possible.

So, what happens to your annual income then?

The equal biggest issue I see with all the above, is the lack of room for tax in the strategy.

On top of the assumptions in growth and serviceability etc, if you did actually pull this off for a decade or so, then let’s hope you never need to sell?

If you refinance and pull money out as a deposit to buy another house, that money is moved from one asset to another. However, the Infinite Equity model in retirement mode, means that you refinance and pull money out to live on.

That money is goooonee.

No tax is paid as it is a refinance and not a classed income.

I am not a pro-tax-guy, but this is surely setting you up for failure.

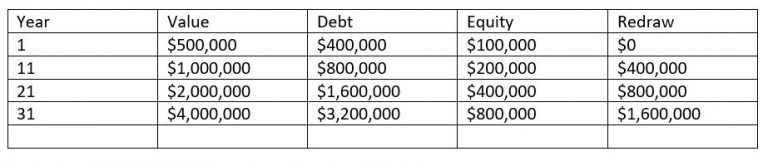

Going back to the example above, property 1 has been held for 10 years and doubled in value.

Bought for $500,000 it is now worth $1,000,000 with a loan of $400,000.

Its refinance time and cost of living has increased so you need to bring in a bit to live on and service your investment portfolio.

You now take the property loan up to $800,000 and live on the $400,000 to run your life and your portfolio.

Next year you do the same thing to property number 2.

Then property number 3 etc.

Let’s look at the numbers on just 1 property:

If we sell in year 32 then it looks like this:

Sale $4,000,000

less costs $200,000 (Agents, marketing, legal)

Net Sale $3,800,000

Minus Debt $3,200,000

Balance $600,000

At this point you might be thinking things look good.

But what about tax?

Using rough napkin style calculations, I come up with the following:

Nett Sale $3,800,000

Initial cost base $500,000

Taxable Balance $3,300,000

CGT exemption $1,650,000

Tax @ 30% $495,000

Your sale balance is $600,000 but your tax bill is $495,000

Leaving you $105,000 when you sell a $4m property. That is a 2.6% on sale price.

Disclaimer: this is totally a napkin formula and does not take into account depreciation, purchase costs, land tax and a myriad of other things.

However, it is based on best case scenario, making it pretty scary if you consider anything like non-lineal growth, inability to finance, changes in tax rules or anything (and everything) else that can negatively impact the financial performance of the properties.

For me, the idea of refinancing for lifestyle support is silly, albeit can be done in a perfect world. (Instead, you should be chasing cashflow from investments for income support)

We don’t live in a perfect world and even if we did, you would need to be 97.4% accurate on your 30-year projections, or else you will be losing money at time of sale.

I am good, but I am not 97.4% accurate over 30-year figure predictions and market performance, good.

Are you?

Just like the Property Cycle, Mortgage Managers and ‘Special Strategies’ like Infinite Equity come and go. The last time I saw this strategy being promoted was about 16 years ago, at exactly the same point in the property cycle.

The second half driven by emotion…

Alex, thanks for your great question!

I hope this has helped you and anyone else thinking about the idea of Infinite Equity.

If you want to secure your financial future using property, then contact us here

or call now on 1300 66 77 89.

Since 2004, Scotty North has been helping people buy the best properties for their needs at prices that simply speak for themselves.

Scotty has been instrumental in bridging the gap between financial planning and traditional real estate transactions through his property advice model.

Scotty North is a Qualified Property Investment Advisor (QPIA), with accreditation’s in financial planning, mortgage broking and real estate.

By carefully considering his clients’ goals and planning for market changes via demographics and trends, Scotty designs a future proof outcome not only specific to the client’s needs but dynamic in its execution with performance indicators and exit strategies built in.